Beyond APTA – the role of software in pension transfer advice:

Last week, we looked at the role of cashflow modelling in DB transfer advice, and the kinds of modelling available. We also looked at why a simple “DB vs SIPP” comparison is not enough, and that we need to ask deeper questions. This week, we’ll look at some of those questions:

- What if the market were to collapse?

- Are you taking too much risk?

- What if you were to die in retirement?

A cashflow model helps show a client whether a DB transfer will allow them to live the life they want, but it’s only by asking difficult questions that we can see if the advice is truly suitable!

Digging deeper…

Risk is a big concern with any DB transfer. One of the primary reasons for advocating NOT transferring out of DB schemes is that they’re cast-iron, guaranteed sources of income in retirement. There’s almost zero exposure to market risk (providing their old employer isn’t owned by Sir Philip Green). The ability to show the effect of a market crash helps illustrate to the client the potential impact not only on their cashflow, but on their lifestyle in retirement!

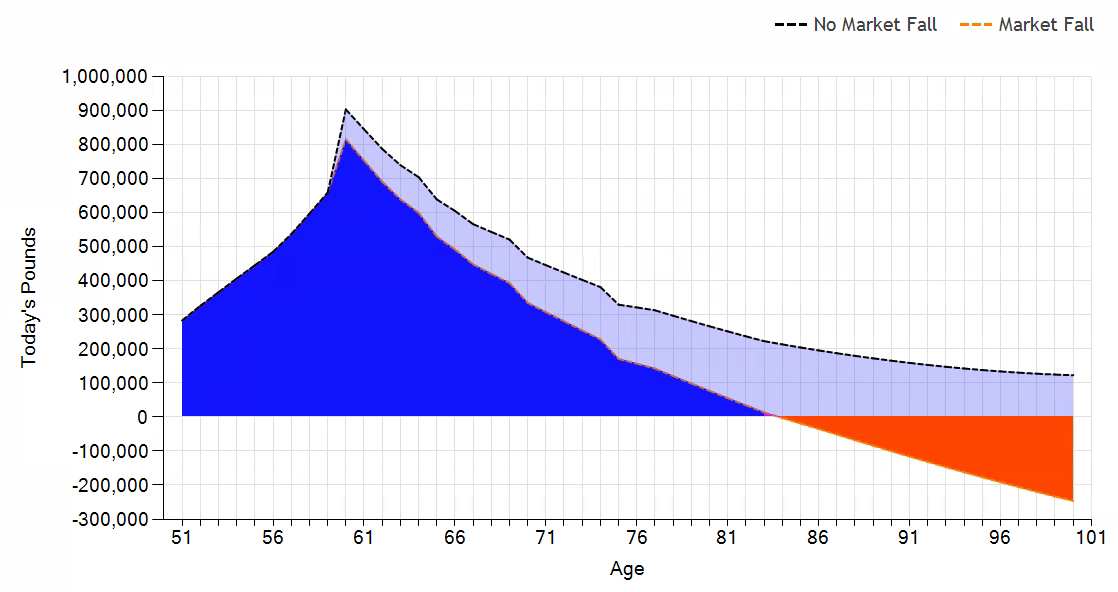

Here’s our capital chart. Remembe

r, this shows Michael’s liquid capital over his lifetime if he were to transfer his pension. He reaches age 100 with around £150,000 capital remaining.

But look what happens to if he were to experience a 30% market fall immediately before retirement:

Suddenly, Michael is £300k short of the lifestyle he wants to live in retirement!

In reality, they wouldn’t REALLY run up a £300k overdraft – planning exercises would take place to prevent this. Therein lies the value of the annual review! But what IS true, and evident from this chart, is that Michael’s retirement lifestyle might be at risk outside his DB scheme.

Let’s de-risk…

OK, so let’s de-risk.

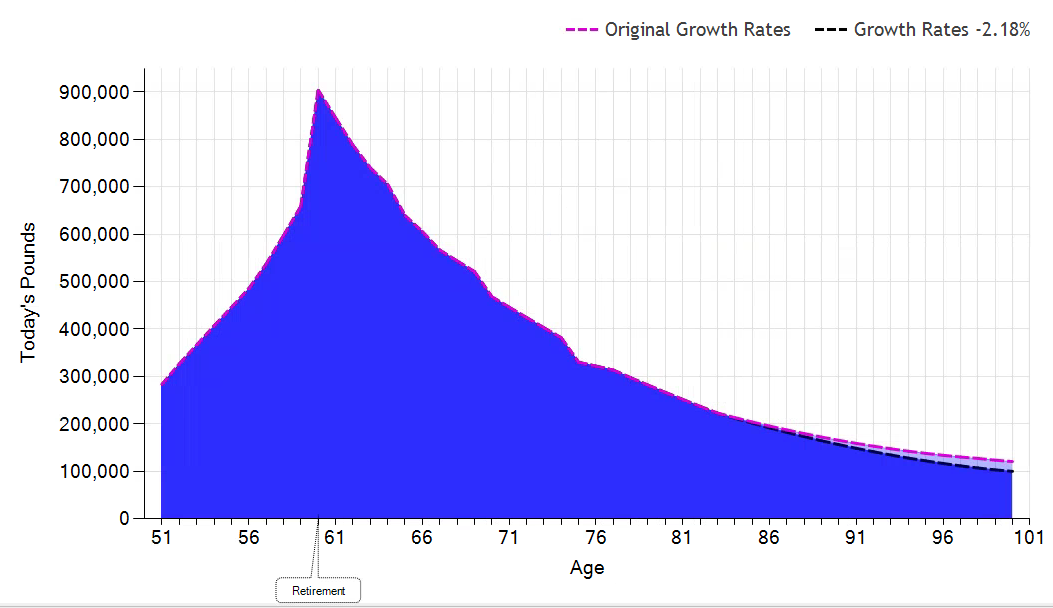

Let’s see the impact of reducing the exposure by moving Michael to a portfolio with lower return, but less risk. In Truth, you can do this really easily using our Growth Calculator.

The Growth Calculator allows you to calculate how much more growth a client needs to achieve in order to meet their cashflow goals… but it also works the other way. If a client has sufficient capital, but is uncomfortable with the level of risk they are exposed to, this handy tool will tell you how much LESS growth they can achieve, without going below a threshold of your choosing.

Let’s see how much growth Michael NEEDS in order to prevent his liquid capital dropping below £100k by age 100:

Michael’s transferred pension, based on his risk profile, is targeting 5% growth. This shows us that he could actually afford to lose 2.18% of this (i.e. target 2.72% return), and still have £100,000 at age 100. Moving to a less volatile portfolio might well help address any concerns about market risk exposure.

Death and taxes!

Historically, one of the key features of DB pensions was their generous death benefits compared to an equivalent personal pension. However, since Pension Freedoms, the playing field has been levelled significantly.

Historically, one of the key features of DB pensions was their generous death benefits compared to an equivalent personal pension. However, since Pension Freedoms, the playing field has been levelled significantly.

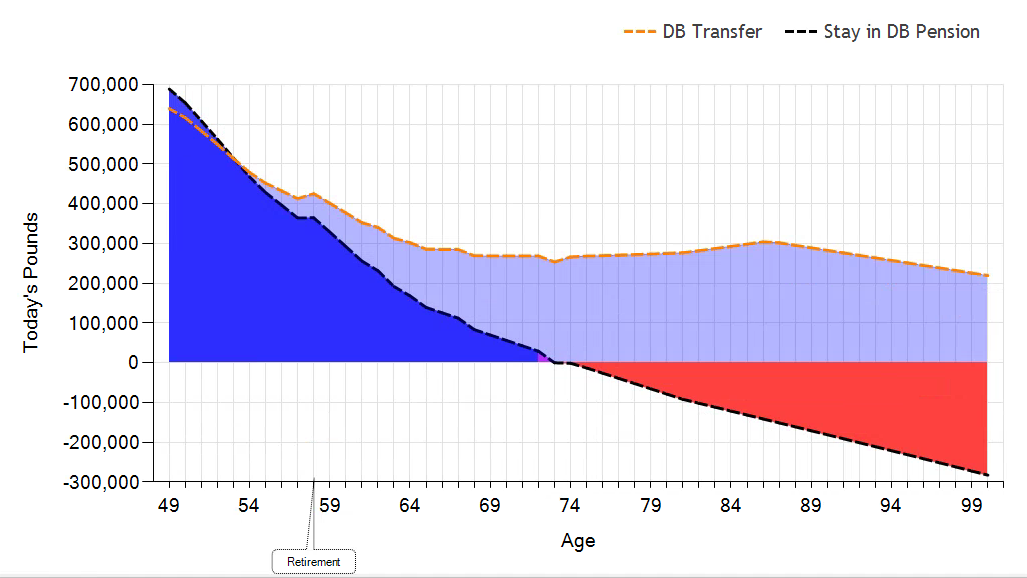

Let’s look at the NHS pension scheme as an example. Depending on when you were a member of the scheme, you might be looking at 5 years’ pension income as a lump sum, followed by 50% of pre-death pension to your nominated beneficiary.

In Michael’s case, he’s taking an income of £12,000 from his DB scheme. Jane, his partner, would receive a lump sum of £60k, then an income of £6k/annum for the rest of her life. This income would potentially be taxable.

The transfer value offered by Michael’s old employer is £420,000. Under Pension Freedoms, Jane would be entitled to all of this as a tax-free lump sum. Alternatively, she could take a tax-free dependent’s drawdown, leaving the pension invested.

Let’s take a look at how these two options compare:

If he were to stay in his DB scheme, Jane would receive a nice lump sum up-front. However the income of £6k/annum isn’t enough to sustain her in retirement. When her state pension kicks in, she starts paying tax on a portion of her income.

If he were to transfer out of his DB scheme, Jane could take £12k per annum tax-free until the pot is depleted (that’s the “bump in the road” at her age 85). She would have sufficient liquid capital to live the life she wants in Michael’s absence.

To find out why we’re the UK’s leading cashflow modelling software, take a look at our website.