I briefly thumbed through the FCA’s response to their consultation paper on Defined Benefit (DB) transfer advice when it was first published last month, but an FP Today article published earlier this month prompted me to review it. The more I read it, the more I am convinced that the FCA have completely missed the point, when it comes to the value cashflow modelling can add to DB transfer advice.

An expensive alternative to Excel!

Following the FCA consultation paper on Appropriate Pension Transfer Analysis (APTA), Prestwood published our white paper Addressing the Pensions Timebomb in November 2017. In this paper we recommend “mandatory use of cashflow modelling to make the consequences [of transferring out of DB pensions] clear to consumers”.

These consequences are various and complex: both negative (sacrificing secure income; exposure to market risk; loss of death/disability benefits) and positive (control and access over pension funds; generous transfer value offers; option to use pensions in IHT planning).

We looked forward, optimistically, to the FCA’s response, and how it would address the complexities of this difficult and often controversial area of advice.

This is the section of the Policy Statement where the FCA discuss the feedback on incorporating cashflow modelling into APTA:

Advisers will be best placed to assess the needs and circumstances of their individual clients. So we do not intend to provide detailed rules and guidance on the relevant elements to include for each individual. We consider that it is for firms to decide whether a critical yield approach remains valid in some circumstances. Firms should be aware of the risks of using critical yield over uncertain future lifetimes where income would not be secure, or where consumers may not understand it.

Firms are not prevented from using cashflow modelling software or any other type of software. However, advisers should consider the part these tools play in explaining the options to individual clients. The limitations of software cannot be used to limit advisers’ responsibility for providing suitable advice.

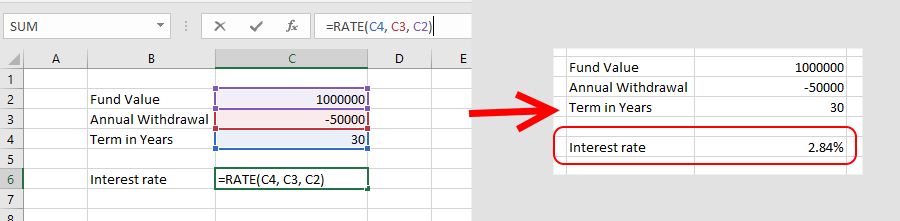

It would appear, from this, that the FCA see the primary role of cashflow modelling in the DB transfer advice process as helping advisers calculate critical yield. If this is all you think you need cashflow modelling software for then don’t waste your money – the “RATE” formula in Excel will do the job for you; so, for that matter, can an investment calculator or your smartphone.

If critical yield approach is only valid “in some circumstances”, surely there should be an alternative suggestion? What exactly does the critical yield approach tell us, what ARE the alternatives, and how can cashflow models help?

Why a critical yield approach is fundamentally flawed

Critical yield is based on trying to create parity between the client’s cashflow were they to remain in their DB pension, and their cashflow if they were to transfer out. What rate of return would the client need in order to replicate the income they would get under their DB pension scheme?

Surely the whole point of transferring out of a DB pension is that the client probably doesn’t want the level of income they would get from their DB pension scheme? If they wanted that exact income, the most prudent course of action would be to advise them to remain in the scheme, where the probability of achieving that level of income is 100%!

Why introduce volatility when success is guaranteed?

The client, in all likelihood, is considering a transfer because they DON’T want to take an escalating income from a date set by a scheme administrator, which will leave them with more income at age 100 (when they aren’t in a position to enjoy it) than at 60 (when they are). They want control of their pension fund, and the freedom to use it as an IHT planning vehicle, or to take ad-hoc withdrawals from it as and when they are required.

Beyond Critical Yield

While a critical yield calculation could, and perhaps should, be a good starting point; this should not be the primary focus of DB transfer advice. Is there any value in comparing one situation the client doesn’t want to be in with another which they equally have no desire to be in?

The primary focus of DB transfer advice should be whether it’s in the client’s best interest to transfer out of their pension scheme. This analysis HAS to take into account what the client’s objectives are – whether that might be enjoying a better lifestyle in early retirement; or shoring away money for their children or grandchildren.

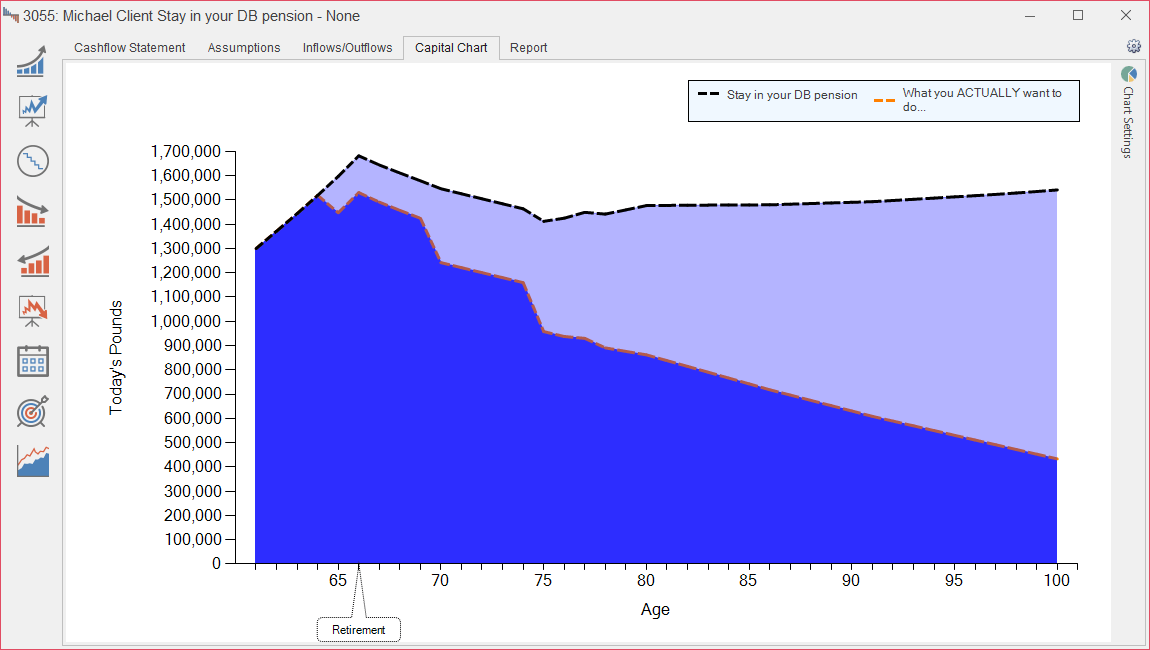

The value of Cashflow modelling is that it helps facilitate the decision making process by illustrating to the client not just the difference between staying in their DB pension and drawing an identical income from a drawdown fund/SIPP, but more importantly the difference between staying in the DB pension and doing what they actually want to do with the rest of their lives.

What Truth’s lifelong cashflow model allows clients to see is a straightforward graphical representation of whether or not they can afford to do what they want to now and for the rest of their lives. Cashflow modelling software, used well, helps the adviser to go far beyond just critical yield. It takes into account clients’ aspirations and allows them to see whether they will be “better off” in a holistic sense, rather than just being better/equally well off in relation to a specific financial transaction.

Why APTA doesn’t go nearly far enough…

The FCA Policy Statement acknowledges that a cashflow model is of some benefit in critical yield illustrations, but ignores the fact that the primary reason for clients wanting to transfer out of their pension is to wrestle control of their funds away from pension scheme administrators.

By providing clients simply with an illustration of how a hypothetical pension could provide the same income as their DB pension, we’re not actually helping them. The value that cashflow modelling can add to DB transfer advice lies in illustrating to clients the difference between where they are now and where they want to be.

But this is just a starting point. APTA addresses market volatility (albeit briefly), but makes little or no reference to the other significant concerns that we should be helping clients to consider: what if they die? What if they are disabled, and in need of long-term care? These are the kind of questions that cashflow modelling software can help you to answer. More importantly, it helps illustrate to the client the wide-reaching implications of what is a complex and important life decision.

Whether you choose to use cashflow modelling software or not, these are the fundamental issues which we should be helping all clients understand before they choose to go ahead with their pension transfer.