A little over 2 years ago, we saw inflation hit a worrying, 20-year high of 8%. With a surge in the usage of cashflow modelling tools amongst financial planning firms, many financial planners found themselves in uncharted territory. Suddenly, clients were querying the assumptions they were using and they simply couldn’t justify them.

Picture this: you are a well-to-do client, concerned about your financial future. It’s April 2022 and the Times has just run an article about inflation hitting 8%. You sit down at a meeting with your financial planner and they attempt to reassure you about your future using a cashflow model. You ask them about the inflation rate they’re using and they tell you it’s 3%. When you ask them why, they hesitate… “let me get back to you on that…”

The problem wasn’t that the assumption was unreasonable, but that many advisers didn’t understand the assumptions they were using. They’d never NEEDED to understand them because clients had never questioned them. Suddenly, advisers started posting on Social Media and adviser forums suggesting changing all cashflow models to use 8% inflation. These posts met with positive responses and we felt the urgent need to challenge this and address a perceived knowledge gap.

Our advice at the time? Do nothing! But were we right to suggest this?

28 months later: we’re now in a position to judge. Did the feared Inflation Apocalypse happen? Was it like a low-budget Danny Boyle movie, where civilisation as we know it was brought to its knees, or was it more of a storm in a teacup?

March 2022 – DON’T PANIC

Let’s set the scene by reminding you of what was going on way back in March 2022. Economically, a lot has happened, since then!

Inflation had just hit 8% for the first time since 1991 and nobody quite knew what it meant. As a lot of firms were fairly new to Cashflow Modelling, they were using assumptions that might have been built into the tools they had purchased, or selected in more stable economic times. Clients were questioning the sanity of modelling using inflation rates that were a fraction of what they were hearing about in the news.

When we saw positive responses from the advice community to posts recommending using a long-term inflation rate of 8%, we felt the need to offer an explanation of long-term measures of inflation that advisers could share with their clients in order to justify the assumptions they were using. We didn’t dictate what people should be doing, but we provided them with the information they would need to come to their own conclusions about what was reasoned and reasonable.

Long-term inflation trends

Our recommendation, at the time, was to use long-term inflation measures as a guide for the assumptions you use in cashflow models. If you’re modelling for 20, 30, or even 40 years of a client’s financial future, it’s reasonable to look at changes over a similar period in the past to justify our assumptions. We looked at the 30-year average of the Retail Prices Index (RPI) which, at the time, was 2.83%. Through simple maths, we explored for how long inflation would need to remain at 2022 levels (or higher) to cause a significant impact on this long-term measure.

Based on OBR and ONS estimates at the time, we speculated that it would take over a year of double-digit inflation to cause a significant shift in long-term rates:

Our conclusion?

we do need to keep a close eye on things. If inflation creeps even higher, there’s a very real chance that by next year your 3% inflation assumption could be a little on the low side. If things stay that way… then maybe it would be prudent to increase your inflation assumption. But only by 1%, not 5%!

The response to this blog was incredible. Not only did we have emails from our customers thanking us for the explanation, we even had messages from competitors telling us the article helped them navigate “difficult conversations with advisers”.

The (un)importance of being right

The maths we used in our original article was based on the Monetary Policy Committe’s aim of bringing inflation back under control within 12 months. As we now know: this didn’t QUITE happen. The government had also hoped that inflation would peak around 10%. This didn’t QUITE happen, either – we saw a peak of 14.2% in October 2022. As a result, our maths was a little bit off. But does this matter?

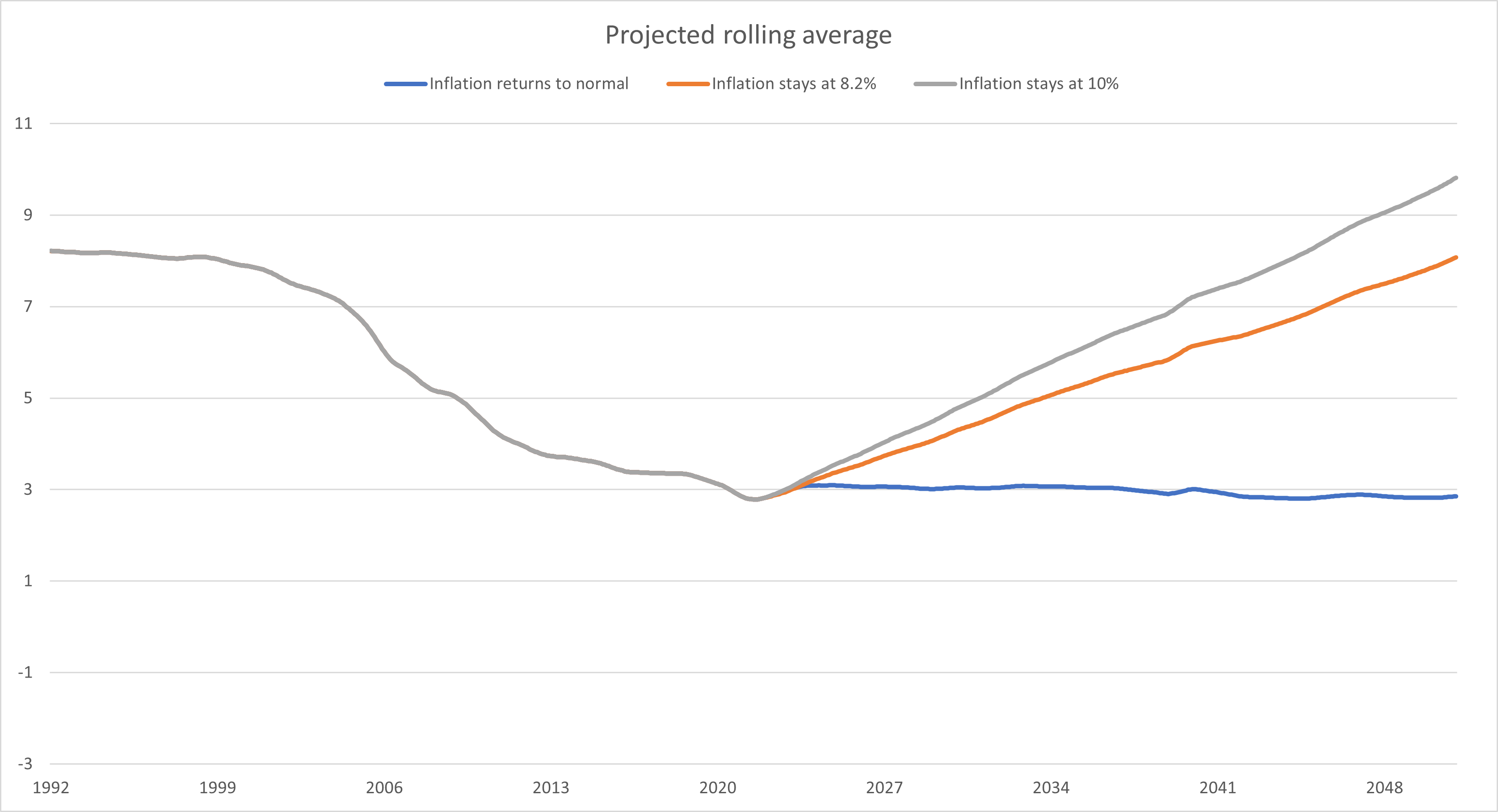

We estimated that it would take 11 months for the 30-year RPI average to reach 3%, but this actually happened in just 8 months! But, as inflation starts to come back down to “normal” levels (latest RPI at time of writing is 4.3% and CPIH 3.8%), I’m sure you’re wondering what two years of high inflation has done to those long-term averages. Well, worry not – I have that answer for you!

In the chart below, we can see the craziness of the last 2 years. In case you can’t, I’ve drawn a big red circle around it!

Compared to the previous 18 years, it’s clear that these were pretty exceptional times.

Let’s try a little experiment. Remember our long-term average, in March 2022, was 2.83%. What do you think it might be, today? Here are a few pointers to think about:

- inflation continued to grow for the next 9 months

- on reaching double-figures, it stayed there for 15 months

- It wasn’t until October 2023 that we dipped back below 8%

I won’t keep you in suspense – the current 30-year average of the RPI is 3.35%. The impact of all of the above: an increase of just 0.53%! And, if that sounds like a lot to you, it’s worth bearing in mind that the long-term average of the RPI had only dipped below 3% in July 2020. The last time it sat at 3.3% was in December 2018, just six years ago. In other words: we aren’t seeing historic highs. The impact of all that craziness is this little blip at the end of the chart below:

But we can’t rest on our laurels – the Cost of Living crisis is far from over. Even with inflation dropping, the disparity between wage growth and prices over the past couple of years is still being felt and the need for ongoing financial planning has never been more apparent. Recognising the importance of long-term assumptions and communicating them to clients helps us meet our Consumer Duty obligations and ensures our advice is received in a way clients understand and can relate to.

Understand your tools

The moral of the story is that being right or wrong isn’t important. What’s important is understanding the tools you use and the assumptions that you (or your tools) make, so that you can justify them to clients when challenged.

While the messages of thanks we received in the aftermath of our original blog made us feel pretty good, that’s far less valuable than the knowledge that we helped fill a knowledge gap. It’s my hope that somewhere out there there’s just one client who, as a result of the information we shared, realised that inflation WASN’T going to stay at 8%. They accepted their adviser’s reasoned, reasonable assumptions and, rather than postpone retirement, they just tightened their belts for a couple of years.

I like to think that they’re currently on a cruise around the Carribean, laughing about how dismal things looked way back in 2022 and how grateful they are that they listened to their financial planner!