At our London User Group last week, conversation turned to our Market Crash Simulator. The room was split between those who swear by this tool, and those who hadn’t yet used it with clients.

Whether you use it to give your clients additional peace-of-mind, or challenge their assumptions and deliver difficult truths, there’s no arguing it’s a hugely powerful planning tool!

Whether you use it to give your clients additional peace-of-mind, or challenge their assumptions and deliver difficult truths, there’s no arguing it’s a hugely powerful planning tool!

My cashflow is fine, why should I care about the Market Crash Simulator?

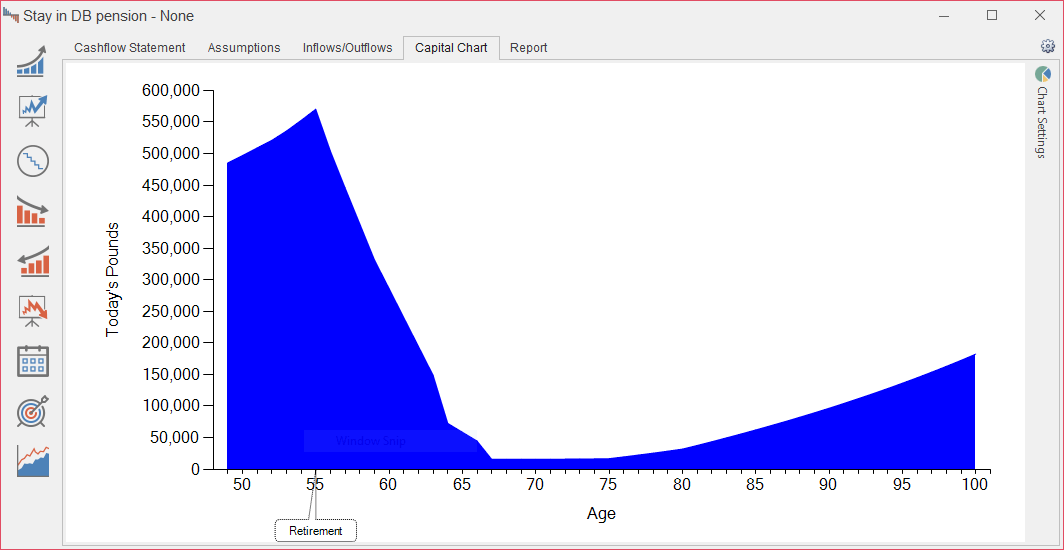

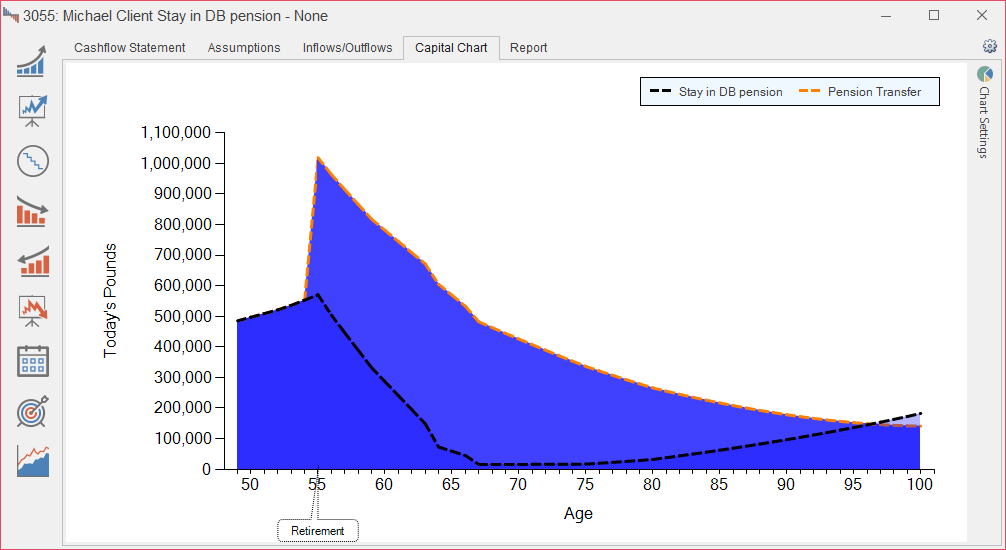

For the uninitiated, this is a Truth® Cashflow Capital Chart – it shows the client’s liquid capital position throughout their life, and whether they have enough money to realise their desired future lifestyle.

This client wants to retire from work at 55, but they’re in a DB pension scheme that doesn’t pay out until they’re 65. They’ve got enough liquid capital to see them through the first 10 years of retirement. From age 65, their generously indexed DB pension kicks in, providing more than enough income in later life.

This client wants to retire from work at 55, but they’re in a DB pension scheme that doesn’t pay out until they’re 65. They’ve got enough liquid capital to see them through the first 10 years of retirement. From age 65, their generously indexed DB pension kicks in, providing more than enough income in later life.

This chart puts me immediately in mind of Abraham Okusanya’s excellent article last year on the myth of “U-shaped” retirement spending. The fact is, clients just don’t need the levels of income in later life that they are worried they might need, and they more than likely need more NOW than they can get their hands on!

In this case, the client has to “just get by” for 10 years in early retirement, then has far too much later on, when they may not be in a position to spend it.

It was the best of times…

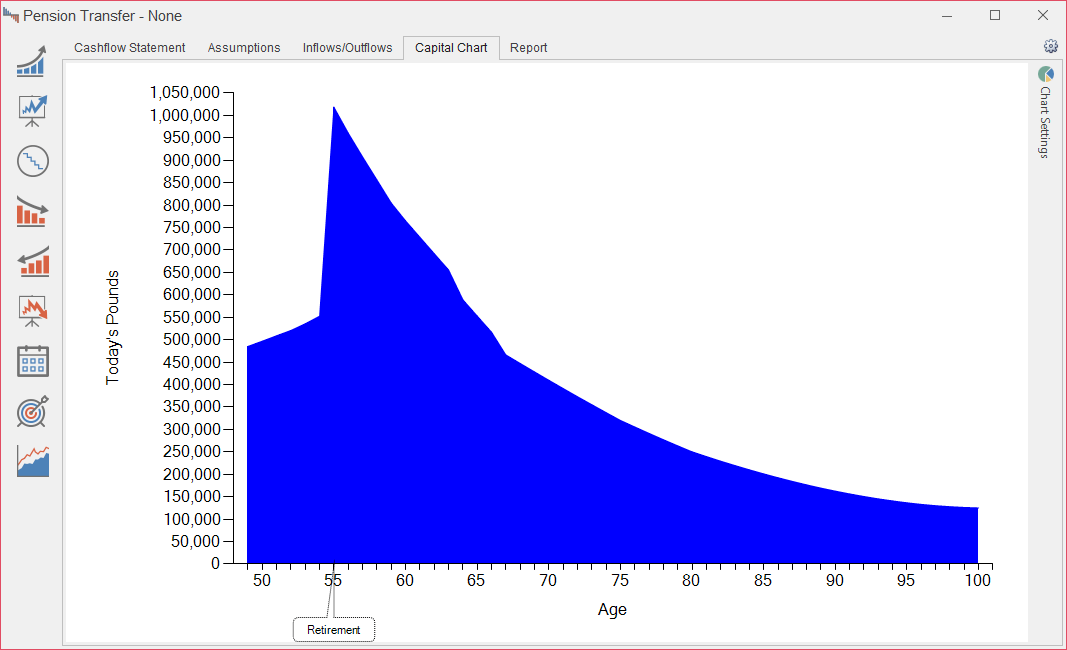

So let’s see how the rest of their life might look if they were to take advantage of the generous DB transfer offer:

Fantastic! They get a lovely injection of capital just when they need it. So what if they have a little bit less income in their 80’s and 90’s – they won’t need it then, will they?

Just to clarify where they’re better or worse off, here’s the two charts overlaid, using our Overlay Charts tool:

You can clearly see that they’re better off transferring, right up to about age 96. If they survive beyond this, they’ve got less to spend, but still die with money in the bank.

You can clearly see that they’re better off transferring, right up to about age 96. If they survive beyond this, they’ve got less to spend, but still die with money in the bank.

So it’s a no-brainer, go ahead with the transfer, right?

Risk and the Deterministic Cashflow

Over the years we’ve had a lot of criticism over the fact that our cashflow model is deterministic. We do offer a Stochastic Calculator, but have no plans to change our fundamental cashflow model, and here’s why.

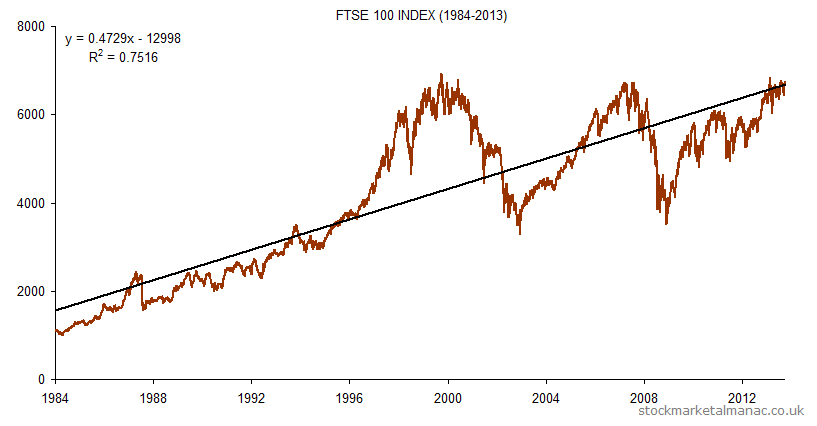

This is the long-term trend of the FTSE 100 index for the first 30 years of it’s life:

That black line in the middle is what would have happened if you’d projected exactly 6.57% linear return over the same period. This is your deterministic assumption – i.e. what you think your clients’ investments are going to do in the long-term. Yes, there will be fluctuations either side, but is it our role, as financial advisers, to attempt to predict the specific behaviour of future markets?

That black line in the middle is what would have happened if you’d projected exactly 6.57% linear return over the same period. This is your deterministic assumption – i.e. what you think your clients’ investments are going to do in the long-term. Yes, there will be fluctuations either side, but is it our role, as financial advisers, to attempt to predict the specific behaviour of future markets?

Julie Lord put this very nicely in her recent article for FP Today:

Investment managers will guess (sorry we mean predict) what will happen to our money next year and many people will be persuaded to act in accordance with these “predictions”… we don’t know what is going to happen in the world in 2018 – and frankly neither, with any certainty, does anyone else!

We’re not saying the client will get exactly x% growth on their pension every year to age 100 (in fact, we doubt very much they will get x% in ANY year), but we’ve made a long-term assumption with the client that it’s going to be somewhere close.

But what if it isn’t?

It was the worst of times…

Sadly the real world isn’t quite so predictable, and doesn’t conform to averages on a day-to-day basis. During the 2007-8 financial crisis, markets fell 21% in a single day. On Black Monday (October 19th 1987) markets fell 28.3%!

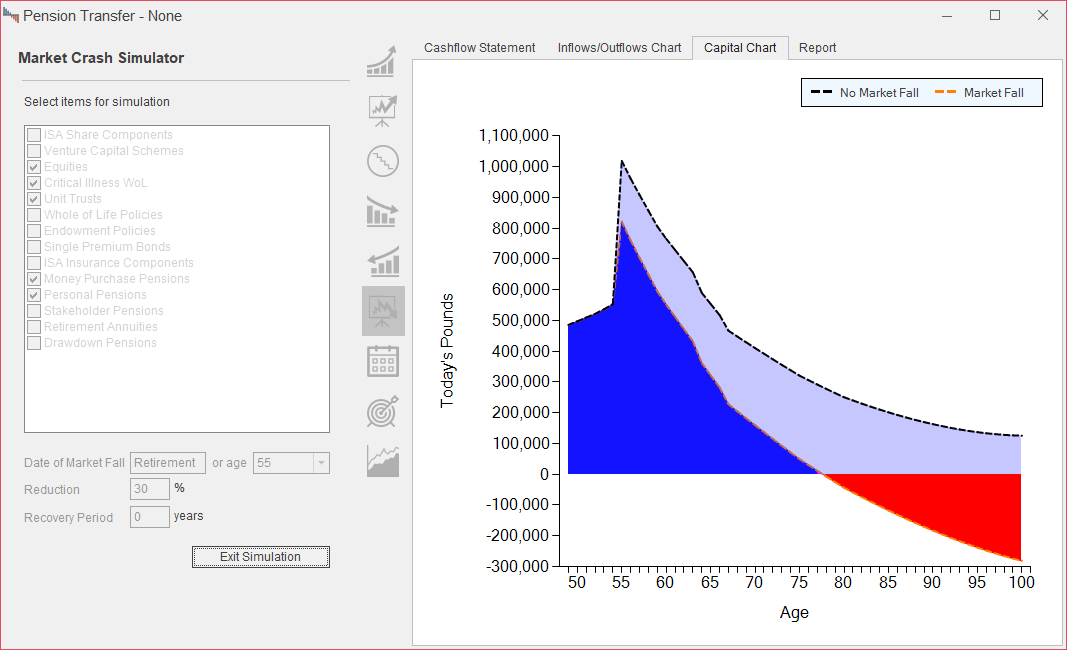

Let’s use the Market Crash Simulator to see what would happen if the client took the DB transfer, got the agreed x% return up to retirement, but then suffered a 30% loss on their portfolio (i.e. worse than either of the crashes mentioned above):

They would run out of money in their late 70s. Suddenly that transfer starts to look like less of a good idea!

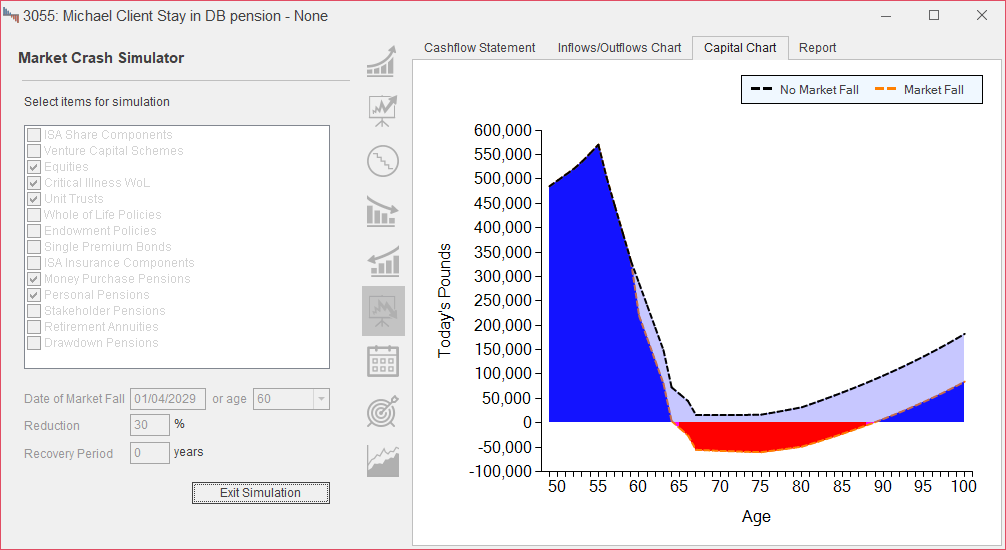

Now let’s look at the same crash if they were to stay in their DB scheme:

They still suffer from the same loss in their other holdings, but their DB pension income is (of course) entirely unaffected. They might need to cut back on their spending for a few years, but the outlook looks significantly more positive due to the security of their DB pension.

They still suffer from the same loss in their other holdings, but their DB pension income is (of course) entirely unaffected. They might need to cut back on their spending for a few years, but the outlook looks significantly more positive due to the security of their DB pension.

Back to the User Group

Consensus in last week’s user group was that the Market Crash Simulator is invaluable not only in increasing client confidence in the robustness of their cashflow projection, but also in challenging the assumptions behind it. Nic Carlton-Smith, of Carlton Smith Private Wealth commented that they use the tool both to empower their clients and to pre-empt future problems:

Prestwood’s Market Crash Simulator helps give our clients further confidence that in the event of a crash, they are still able to maintain their desired spending levels. This has 2 large benefits, the first is that our clients have extra peace of mind on their financial security and the second is that we don’t get many (if any) phone calls when the markets do take a dip.

So what?

A single cashflow chart can never capture all the intricacies of a client’s specific situation. A DB pension transfer might benefit them short-term, based on current assumptions, but what if…?

What if they lose half their portfolio overnight?

What if they die?

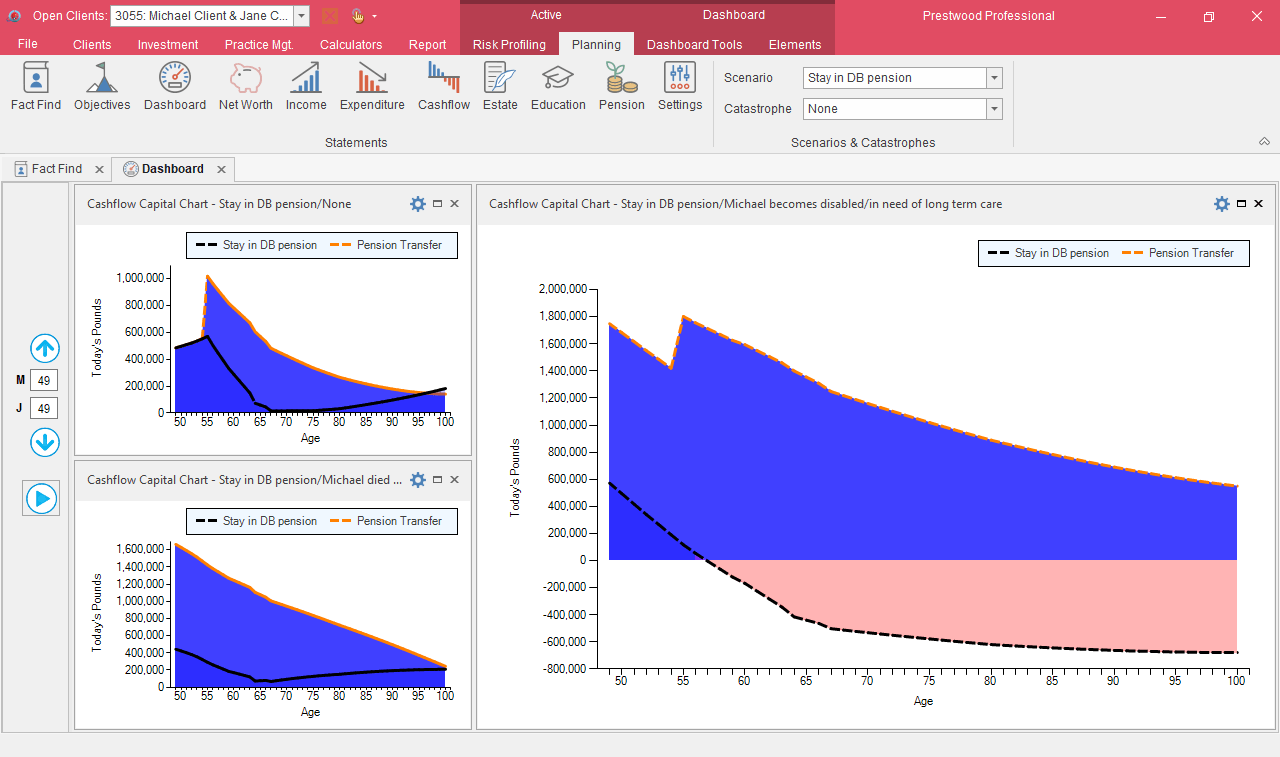

What if they were disabled, and in need of long-term care?

Thankfully, Truth® allows you to model all of these hypotheticals, and many more, directly from the Cashflow. We don’t just help you look at whether your client is “better off” in or out of their DB scheme, but we try to help you provide holistic advice and a comprehensive service to your clients.

You can even use our handy Dashboard tool to show your client all of these hypotheticals in one place!

As the old saying goes: “hope for the best, plan for the worst”. Although we’re hoping for x% growth (on average), and a long, happy, healthy retirement, planners should at the very least make clients aware of what could happen.

As the old saying goes: “hope for the best, plan for the worst”. Although we’re hoping for x% growth (on average), and a long, happy, healthy retirement, planners should at the very least make clients aware of what could happen.

Truth® can help clients visualise the impact of “the worst”, and so helps you plan for it. These charts help to start that conversation about how they may feel if something bad does happen, and consider whether they can handle it financially and emotionally. Just because we can’t accurately predict a crash, or how bad it might be, that doesn’t mean we should opt not to discuss it and educate our clients about how these what-ifs might impact on the rest of their life. All the while, you’re protecting your business by creating a robust compliance audit trail.

By pre-empting the worst-case scenarios, we can reassure clients and give them the peace-of-mind that can only come from knowing that we’re trying to help them plan for their financial future, however that might look. We’ll continue to hope for the best, but if the worst might happen, we’ve got it covered.